TL;DR:

- Nearly half of homeowners finance HVAC systems to manage high costs and improve home comfort.

- Options include personal loans, manufacturer plans, home equity, credit cards, and leasing.

- Carefully compare terms, total costs, and long-term benefits before choosing an HVAC financing method.

Nearly half of all homeowners finance their HVAC systems rather than paying the full cost upfront, which means you are far from alone if a new furnace or AC replacement feels out of reach right now. For Kansas City homeowners, HVAC costs can run anywhere from a few hundred dollars for a repair to over $10,000 for a full system installation. Financing turns that large number into a manageable monthly payment, putting better comfort and lower energy bills within reach today. This guide walks you through the main financing types, how to apply, and how to decide which option fits your budget and goals.

Table of Contents

- Understanding HVAC financing basics

- Common HVAC financing options explained

- When is HVAC financing worth it?

- How to apply for HVAC financing: step-by-step

- A practical perspective on HVAC financing decisions

- Unlock affordable comfort with Kansas City HVAC experts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple financing options | Kansas City homeowners can choose from loans, leases, and promotional offers to fund HVAC upgrades. |

| Efficiency offsets cost | Energy savings from new HVAC systems can help cover monthly financing payments over time. |

| Ownership has advantages | Owning a system with a loan can qualify you for tax credits and increase home value. |

| Smart shopping is critical | Always compare total costs, terms, and potential energy savings before committing to any HVAC financing. |

Understanding HVAC financing basics

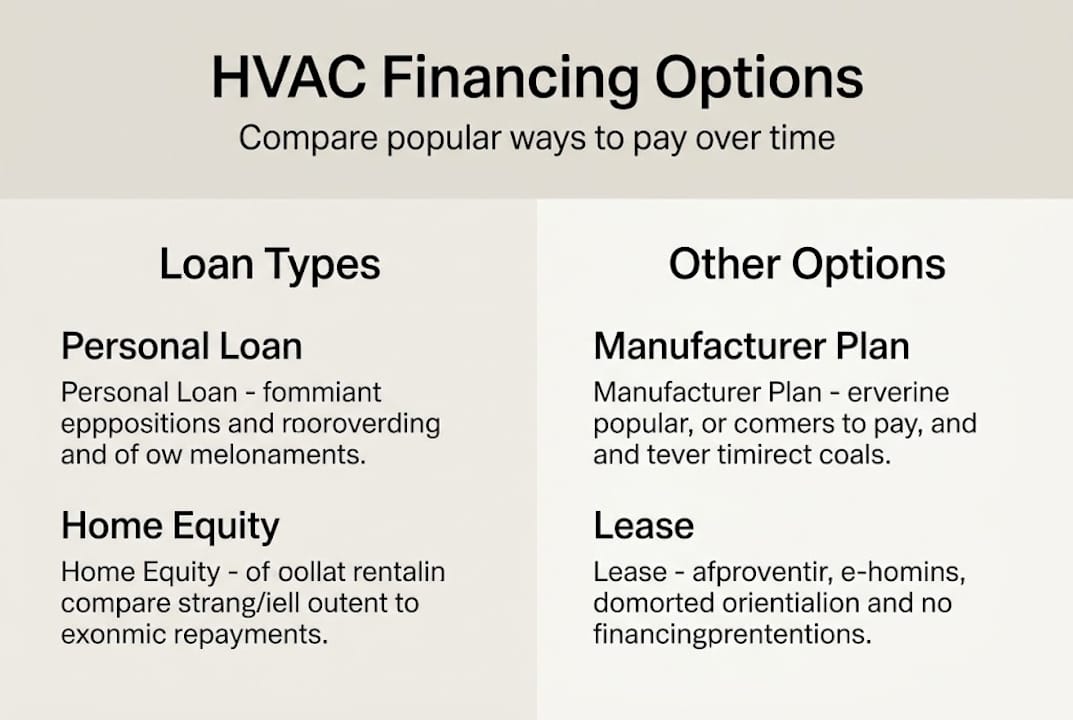

HVAC financing is simply a way to spread the cost of heating and cooling work over time instead of paying everything at once. It can take several forms: a personal loan, a manufacturer payment plan, a credit line, or a promotional offer through your HVAC contractor. Each option has its own terms, interest rates, and repayment timelines, so understanding the differences matters before you sign anything.

The most common reasons Kansas City homeowners turn to financing include emergency system failures in the middle of summer or winter, planned upgrades to higher-efficiency equipment, and large repairs that exceed what savings can cover. Understanding how HVAC maintenance impacts financing can also help you avoid situations where a neglected system forces a costly emergency decision.

Here are the major financing types you will encounter:

- Personal loans: Unsecured or secured loans from banks, credit unions, or online lenders. Funds arrive quickly, and you own the equipment outright.

- Manufacturer financing: Offered through brands like Carrier or Lennox, often with promotional rates. Approval can be easier, but you may be limited to specific equipment lines.

- Home equity loans or lines of credit (HELOC): Borrow against your home’s value for lower interest rates and longer repayment terms.

- Credit cards: Useful in emergencies, especially with a 0% introductory period, but high ongoing rates if not paid off in time.

- Contractor payment plans: Some HVAC companies offer in-house financing with flexible terms directly through their service agreements.

| Financing type | Typical rate | Ownership | Best for |

|---|---|---|---|

| Personal loan | 7-20% | Yes | Quick funding, any credit |

| Manufacturer plan | 0-15% promo | Yes | Brand-specific upgrades |

| HELOC | 6-10% | Yes | Large projects, good credit |

| Credit card | 18-29% | Yes | Small or emergency costs |

| Lease | Fixed monthly | No | Low upfront, short-term |

Energy-efficient upgrades are one area where upgrading your HVAC can actually offset a portion of your monthly loan payment through lower utility bills. 40-50% of homeowners finance HVAC systems because the math often works in their favor when energy savings are factored in.

Pro Tip: When comparing financing offers, look beyond the interest rate. Check the repayment term, any origination fees, and whether there is a prepayment penalty if you want to pay it off early.

Common HVAC financing options explained

With the basics in mind, let’s compare your top financing options side by side so you can see exactly what each one means for your wallet.

Personal loans are the most flexible choice. You borrow a fixed amount, repay it over a set term, and own the equipment from day one. If your credit score is strong, you can find competitive rates. Weaker credit means higher rates, but funding is still possible.

Manufacturer financing programs, offered through brands partnered with HVAC contractors, often feature promotional periods like 12 or 18 months at 0% interest. The catch is that approval may favor buyers who choose specific product lines, limiting your options. Still, for homeowners committed to a particular brand, these programs offer real value.

Home equity loans and HELOCs give you access to your home’s built-up value at relatively low interest rates. Terms can stretch to 10 or 20 years, keeping monthly payments small. The trade-off is real: your home is the collateral, so missed payments carry serious consequences.

Credit cards work well for smaller repairs or when you can pay off the balance within a 0% promotional window. Outside of that window, rates can climb above 25%, making them a costly long-term choice for large system replacements.

Leasing is a newer option in the HVAC market. Monthly payments are low, and maintenance is sometimes included. However, as ownership through loans can enable tax credits and build home equity, leasing offers neither of those benefits. You also may face restrictions on upgrades and could pay more in total over the lease term than you would have paid to own the system outright.

“When you own your HVAC system through a loan, you may qualify for federal energy efficiency tax credits and build home equity. A lease keeps payments low but transfers those long-term financial benefits to the leasing company instead of you.” — GoodLeap HVAC Financing Insights

For homeowners focused on energy efficient HVAC benefits, ownership through a loan or home equity product is typically the smarter long-term move. The KC energy efficient HVAC guide breaks down which systems qualify for the most savings in our region.

When is HVAC financing worth it?

But with all these options, how do you know if HVAC financing is right for your particular situation?

Financing makes the most sense in these scenarios:

- Emergency replacement: Your system fails in January and you have no savings buffer. Financing keeps your family warm without draining other financial resources.

- High-efficiency upgrades: A new high-efficiency system can cut utility bills by 20-50% in Kansas City homes, and those savings can partially or fully offset the monthly payment.

- 0% promotional offers: When a manufacturer or contractor offers true 0% financing with no deferred interest, you are essentially borrowing money for free.

- Tax credit eligibility: Owning a qualifying high-efficiency system may make you eligible for federal tax credits, reducing the real cost of the upgrade.

- Avoiding depleting emergency savings: Keeping your savings intact for true emergencies while financing a planned upgrade is a reasonable financial strategy.

Financing is less ideal when interest rates are high and you have cash available, when fees make the total cost significantly higher than the sticker price, or when you are considering a lease that locks you into a long-term agreement without ownership benefits. Financing is especially valuable for efficiency upgrades that generate energy savings, but it should be avoided when high interest erodes those gains.

Knowing when to retrofit for efficiency versus replacing a system entirely also affects whether financing is the right call. For full replacements, the KC installation guide can help you estimate total project costs before you apply.

Pro Tip: Run a simple comparison. Take your estimated monthly loan payment and subtract your projected monthly energy savings. If the net cost is low or close to zero, financing a high-efficiency system is almost always worth it.

How to apply for HVAC financing: step-by-step

Once you have decided financing is right for you, here is how to get started in a few clear steps.

- Get accurate estimates first. Before applying, collect at least two written estimates from licensed HVAC contractors. Getting accurate KC HVAC estimates ensures you borrow only what you need and can compare contractor financing offers fairly.

- Check your credit score. Your credit score affects the rates and terms you qualify for. Pull a free report and review it for errors before applying. HVAC financing options are tiered based on your credit and income, so knowing where you stand helps you shop strategically.

- Gather your documents. Lenders typically ask for proof of income, recent pay stubs or tax returns, identification, and your contractor’s estimate or invoice.

- Compare at least three offers. Apply to your HVAC contractor’s financing program, a local bank or credit union, and at least one online lender. Compare total cost, not just monthly payment.

- Read the fine print before signing. Pay close attention to whether a 0% offer includes deferred interest. With deferred interest, if you do not pay off the full balance by the end of the promotional period, all the interest that accumulated gets added back to your balance at once.

- Confirm installation details. Once approved, coordinate with your contractor on installing a new HVAC system so the work begins promptly and your new equipment is covered under warranty from day one.

Pro Tip: Deferred interest is not the same as 0% interest. Always ask your lender directly: “Is this true 0% interest, or is interest deferred?” The answer changes the total cost significantly.

A practical perspective on HVAC financing decisions

Most financing guides stop at listing your options. But after working with Kansas City homeowners for over 70 years, we have seen one pattern repeat itself: people focus on the monthly payment and forget to calculate the total cost of financing.

A $8,000 system financed at 15% over five years costs you nearly $11,000 by the time you are done. That extra $3,000 matters. It is not a reason to avoid financing, but it is a reason to shop hard for better terms.

Leases look attractive on paper because the monthly number is small. But you never own the equipment, you cannot claim tax credits, and you may pay more over five years than the system was worth. We have seen homeowners locked into lease agreements that prevented them from upgrading to better technology when it became available.

Home equity lines work well for homeowners with stable income and solid credit. For anyone with variable income or job uncertainty, using your home as collateral for an HVAC upgrade carries real risk.

The honest truth is this: if you can pay cash and the system is not an emergency, ownership gives you the best return. But if financing means you get a high-efficiency system now that delivers energy savings with efficient HVAC for the next 15 years, it is often the smarter long-term move. Choose by what maximizes your total comfort and savings over the system’s lifetime, not just today’s monthly number.

Unlock affordable comfort with Kansas City HVAC experts

Ready to take the next step toward a comfortable, energy-saving home? KC Air Control has served Kansas City homeowners for over 70 years, and we make it easy to explore financing, get accurate estimates, and find the right system for your budget.

Whether you need to understand what HVAC means for home comfort, schedule a trusted furnace repair, or book expert AC repair, our team is ready to help. We offer flexible financing options, upfront pricing, and the kind of reliable workmanship that Kansas City families have counted on for generations. Contact us today to schedule your estimate and find a payment plan that works for you.

Frequently asked questions

How does HVAC financing affect my credit score?

Applying for HVAC financing typically involves a hard credit inquiry, which can cause a small, temporary dip in your score. Financing is tiered by credit and income, so consistent on-time payments can actually improve your score over time.

Can I finance energy-efficient HVAC upgrades in Kansas City?

Yes, most Kansas City HVAC providers offer financing specifically for high-efficiency systems, and energy savings from upgrades can lower your net monthly cost by reducing utility bills significantly.

What is the difference between HVAC loans and leases?

Loans give you ownership of the equipment, potential tax credits, and home equity benefits, while leases offer lower monthly payments but no ownership and typically a higher total cost over time.

Are there risks to 0% HVAC financing offers?

Yes. Many 0% offers include deferred interest, meaning if you do not pay the full balance before the promotional period ends, all accumulated interest is added back to your balance at once, which can be a significant surprise charge.

Recommended

- HVAC maintenance affects financing for Kansas City homes – KC Air Control – Heating & Cooling

- How to choose the right HVAC system for your KC home – KC Air Control – Heating & Cooling

- Energy efficient HVAC installation guide for KC homeowners – KC Air Control – Heating & Cooling

- HVAC estimates in Kansas City: 2026 homeowner guide – KC Air Control – Heating & Cooling