TL;DR:

- Replacing or upgrading your HVAC system can improve comfort and efficiency, with financing options making it affordable. These programs spread costs through fixed monthly payments, offering quick installation and immediate savings on energy bills. Pairing rebates and tax credits with financing reduces overall costs, making energy-efficient upgrades financially practical for Kansas City homeowners.

Replacing or upgrading your HVAC system is one of the smartest moves you can make as a Kansas City homeowner, but the price tag can stop you cold. A new high-efficiency system can run anywhere from $5,000 to $15,000 or more, depending on your home’s size and the equipment you choose. The good news is that you don’t need a large savings account to make it happen. HVAC financing helps Kansas City homeowners fund replacements and upgrades without draining cash, enabling faster comfort restoration and access to higher-efficiency equipment that would otherwise be unaffordable upfront. This guide walks you through how financing works, which programs are available locally, and how to combine incentives to keep your costs as low as possible.

Table of Contents

- How HVAC financing empowers Kansas City homeowners

- Types of HVAC financing: banks, utility programs, and pay-as-you-save

- Stacking incentives: lower out-of-pocket costs with rebates and tax credits

- Realistic savings: do HVAC upgrades pay off even after financing?

- Our take: what most guides miss about HVAC financing in Kansas City

- Upgrade your comfort: expert HVAC support and financing in Kansas City

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Monthly payments, not cash | Financing lets you upgrade comfort and efficiency without needing all the money upfront. |

| Stack incentives for savings | Combining rebates and credits with financing reduces both your total and monthly costs. |

| Flexible financing options | Bank loans, utility bill programs, and pay-as-you-save plans offer different paths for all credit levels. |

| Savings still add up | New, high-efficiency HVAC systems can lower your energy bills even after factoring in financing payments. |

| Review terms carefully | Always check program rules, interest rates, and transfer conditions before you sign any agreement. |

How HVAC financing empowers Kansas City homeowners

Now that you’ve seen why cash isn’t everything, let’s dig into how financing puts new systems within reach for KC homeowners.

When your furnace quits in January or your air conditioner gives out in a July heat wave, waiting months to save enough money is not a realistic option. HVAC financing solves this problem by spreading a large, one-time expense into predictable monthly payments you can actually plan around. Instead of watching your family sweat through August while you scramble to pull together thousands of dollars, you can have a new system installed and running within days.

The smart HVAC financing options available to Kansas City homeowners cover a wide range of situations. Some programs are designed for homeowners with excellent credit who want low interest rates on personal loans. Others, which we’ll cover in the next section, are tied directly to your utility bill and require no credit check at all. Both types give you immediate access to upgraded comfort and efficiency, which means you start saving on energy bills right away rather than waiting until you’ve saved enough to pay cash.

Here’s why that matters. High-efficiency systems, rated at 16 SEER2 (Seasonal Energy Efficiency Ratio 2, the current federal efficiency rating standard) or higher, cost more upfront than basic models. Many homeowners settle for a lower-tier unit simply because it’s what they can afford at the moment. With financing, you can afford the better unit, which typically saves more money each month and has a longer useful life. When you consider the total cost over ten to fifteen years, upgrading for energy savings often makes more financial sense than buying cheap and replacing sooner.

- Financing covers the full system cost, including installation labor

- Monthly payments are fixed, making budgeting straightforward

- You get immediate comfort while the system pays for itself over time

- Higher-efficiency units qualify for more rebates and tax credits

- Many programs offer 0% promotional interest for a set period

“Many KC homeowners see comfort restored quickly when using local financing programs, often within a week of applying, without any large upfront payment required.”

Pro Tip: When comparing financed systems, don’t just look at the purchase price. Focus on equipment with strong energy ratings and manufacturer warranties. A better unit financed over 60 months may cost the same monthly payment as a basic unit financed over 36 months, but will deliver lower energy bills and last years longer.

Types of HVAC financing: banks, utility programs, and pay-as-you-save

Understanding the basics, let’s compare the main ways Kansas City homeowners can finance upgrades.

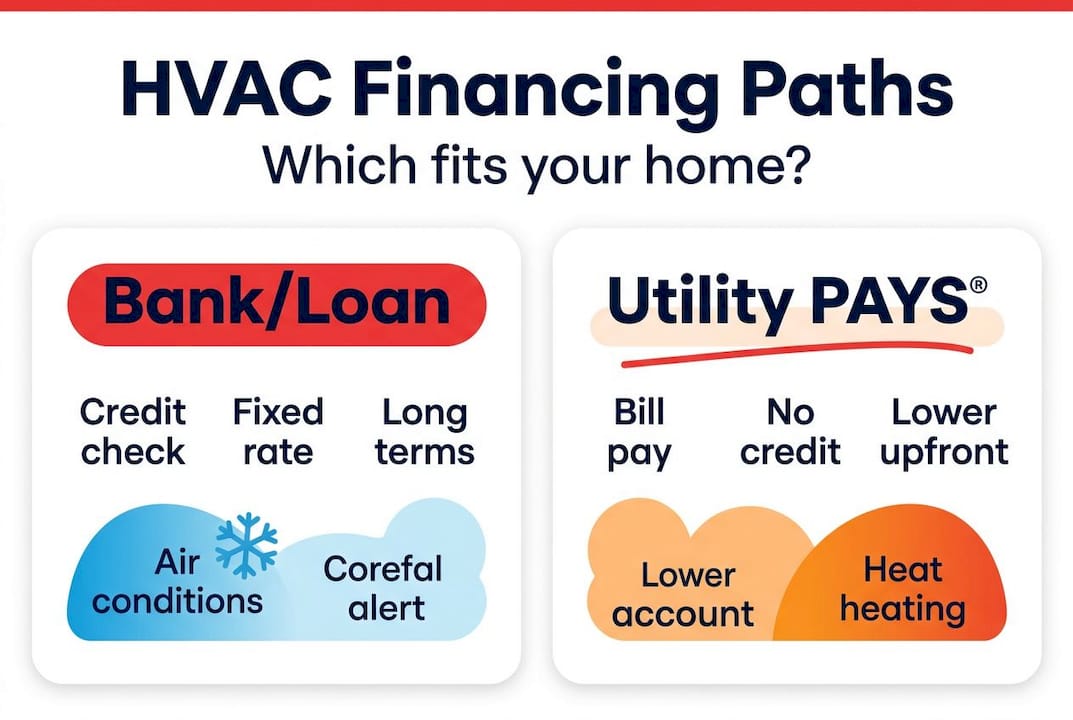

There are three main financing paths available to you as a Kansas City homeowner. Each one works differently, comes with its own set of eligibility requirements, and suits different situations. Knowing the differences helps you choose the right fit for your credit profile, your home ownership plans, and your comfort timeline.

Traditional bank or credit union loans work the way most personal loans do. You apply, the lender checks your credit score, and if approved, you receive funds you use to pay your contractor. These loans often offer competitive interest rates for borrowers with good to excellent credit, and repayment is tied to you personally, not your home. The downside is that the process takes time, and homeowners with less-than-perfect credit may not qualify or may face higher interest rates.

Utility-based programs like Evergy’s FastTrack HVAC PAYS® take a completely different approach. The Evergy PAYS® program offers customized upgrade financing plans that repay upgrade costs through a fixed monthly charge on your Evergy bill, with no credit checks required. This is a significant advantage for homeowners who might not qualify for traditional financing. Because the repayment is handled through your utility account, it doesn’t show up as personal debt on your credit report.

The Evergy FastTrack PAYS® structure also includes a unique feature: utility-run financing can reduce upfront costs by tying repayment to the utility bill rather than the homeowner’s credit. This pay-as-you-save model means the financial obligation can stay with the home and the utility account rather than following you personally.

Here is a straightforward comparison of the three main options:

| Financing type | Credit check required | Repayment tied to | Stays with home if you sell |

|---|---|---|---|

| Bank or credit union loan | Yes | Borrower personally | No |

| Contractor financing | Usually yes | Borrower personally | No |

| Evergy PAYS® utility program | No | Utility account/home | Yes (in some cases) |

Pros and cons at a glance:

- Bank loans: Low rates for good credit, but slow approval and credit-dependent

- Contractor financing: Convenient and fast, but interest rates vary widely

- Evergy PAYS®: No credit check and bill-based, but eligibility requirements apply and not all homes qualify

When applying for HVAC financing, gather your utility account information, home details, and recent energy bills before you start. This speeds up the process for utility-based programs significantly.

Stacking incentives: lower out-of-pocket costs with rebates and tax credits

Now, let’s see how you can make the most of financing by pairing it with available incentives.

Financing covers the cost of your upgrade, but rebates and tax credits reduce what you need to finance in the first place. Using both together is the most effective strategy for Kansas City homeowners who want maximum savings with minimum monthly burden. Stacking incentives means combining utility rebates, manufacturer promotions, and federal tax credits so the total financed amount shrinks before you sign anything.

The federal Inflation Reduction Act, for example, offers tax credits of up to 30% on qualifying energy-efficient HVAC equipment. On a $10,000 system, that’s $3,000 back at tax time. Evergy and other local utilities offer their own rebates on top of that. When stacked properly, you might reduce a $10,000 project to an effective cost of $6,500 or less before financing begins.

Here’s the smart workflow for stacking your savings:

- Choose eligible equipment. Select systems that meet both federal tax credit requirements and Evergy’s rebate program qualifications. Your HVAC contractor can confirm which models qualify.

- Get rebate confirmation in writing. Contact your utility provider and request documentation of any rebates available before you sign a contract.

- Calculate your real out-of-pocket cost. Subtract confirmed rebates and estimated tax credits from the system price. This is the actual amount you need to finance.

- Arrange financing on the reduced amount. Apply for financing based on your net cost, not the sticker price. This lowers your monthly payment and total interest paid.

- Keep records for your tax return. Save all documentation for the 25C or 25D tax credit forms, depending on your equipment type.

“Kansas City utility and manufacturer programs can provide upfront rebates of $1,000 or more, and when combined with the federal tax credit, total savings can reach several thousand dollars on a qualifying system.”

Pro Tip: Always confirm incentive eligibility before signing a finance contract. Rebate programs change regularly, and some have funding caps that run out mid-year. Locking in your rebate confirmation early protects your savings.

For additional HVAC budgeting tips tailored to Kansas City homes, or to explore the full details of energy-efficient HVAC installation, we have resources that walk you through the full planning process. You can also find broader context about energy-efficient home design that pairs well with an HVAC upgrade strategy.

Realistic savings: do HVAC upgrades pay off even after financing?

You may wonder if upgrades actually pay off after financing, so let’s look at the Kansas City numbers.

This is the question every practical homeowner should ask. The honest answer is: yes, for most Kansas City households, the energy savings from a high-efficiency system are real enough to offset the financing costs, often from the very first month.

According to a local HVAC contractor’s description of the Evergy FastTrack program, homeowners can see about 17% lower energy bills even after making their financing payments. That’s a meaningful number when you consider that the average Kansas City household spends roughly $1,800 to $2,200 per year on heating and cooling. A 17% reduction works out to $300 to $375 in annual savings, which is real money in your pocket every year for the life of the system.

Here’s what that looks like in practical terms:

| Scenario | Monthly energy bill | Monthly financing payment | Net monthly change |

|---|---|---|---|

| Old system, no financing | $175 | $0 | Baseline |

| New efficient system, with financing | $145 | $80 | +$50/month |

| New efficient system, financing paid off | $145 | $0 | Saves $30/month |

The middle row shows the honest picture during the financing period. You will likely pay slightly more per month while the loan is active. But once financing is paid off, the savings become purely positive. And with energy-efficient HVAC systems built to last 15 to 20 years, those long-term savings add up significantly.

Results will vary based on your home’s size, insulation quality, and how you use your system. But the trend is consistent: modern high-efficiency equipment uses less energy than older systems, and the gap in monthly energy costs helps offset what you pay to finance the upgrade.

Our take: what most guides miss about HVAC financing in Kansas City

You’ve seen the numbers and options, so what’s the bottom line from our perspective?

Most HVAC financing guides stop at listing the options and pointing out the savings. What they don’t tell you is where homeowners actually get burned, and it’s usually in the details of the financing agreement itself, not the equipment choice.

Deferred-interest financing is one of the most common traps. These promotional offers are advertised as “0% financing for 18 months,” which sounds great. But if you don’t pay off the entire balance before the promotional period ends, you can be charged all the interest that would have accrued from the beginning, retroactively. That can add hundreds of dollars to your total cost overnight. Read every line of your financing agreement, especially the section on what happens when the promotional rate expires.

The pay-as-you-save model through Evergy’s PAYS® program has its own nuance worth understanding before you sign up. The repayment can stay attached to the home’s utility account rather than the borrower, which may matter significantly if you plan to sell your home during the repayment period. This could be an advantage if the buyer is willing to assume the obligation, but it could also complicate your sale if not disclosed properly. Always review what happens to the repayment obligation when the home changes hands.

The total cost of financing matters more than the monthly payment. Two loans with the same monthly payment can have very different total costs depending on the interest rate and term length. A 48-month loan at 9.9% interest costs significantly more overall than a 36-month loan at 6.9%, even if the monthly difference feels small.

Don’t forget that HVAC maintenance directly affects the long-term value of your financed system. A high-efficiency unit that isn’t maintained will lose efficiency and fail sooner, undermining both your energy savings and your investment. Annual tune-ups are not optional when you’ve financed a system. They protect the warranty and keep the equipment performing at the level you paid for.

Our honest advice: financing is a genuinely smart tool when the terms are favorable and you go in with clear expectations. It is not a great idea when you’re chasing a low monthly payment without reading the full contract.

Upgrade your comfort: expert HVAC support and financing in Kansas City

If you’re ready to explore your options, here’s how you can take the next step toward comfort and savings.

At KC Air Control, we’ve been helping Kansas City homeowners find the right heating and cooling solutions for over 70 years. We understand that every household’s situation is different, and that financing is not one-size-fits-all. Whether you’re replacing a failing furnace, upgrading to a more efficient air conditioner, or improving your home comfort with better indoor air quality equipment, we’re here to walk you through your options.

Our team can help you identify qualifying equipment, connect you with available rebates, and explain which financing programs work best for your credit profile and goals. We also offer guidance on HVAC maintenance to protect your investment over time. If you’re ready to start saving on energy bills and improving your home’s comfort, contact KC Air Control today to schedule a consultation. We’ll help you make a confident, informed decision without any pressure.

Frequently asked questions

How does HVAC financing work in Kansas City?

Most programs let you split a large HVAC expense into monthly payments, often paired with local rebates and utility incentives to reduce your overall costs. As noted by local financing resources, financing enables faster access to comfort and higher-efficiency equipment without requiring a large upfront payment.

What’s unique about Evergy’s PAYS® HVAC financing?

You repay through your Evergy utility bill with no credit check required, and in some cases, the repayment obligation stays with the home rather than following you personally if you move. The Evergy PAYS® program is specifically designed to remove credit barriers for qualifying Kansas City homeowners.

Can I use both utility rebates and financing for my HVAC upgrade?

Yes, pairing rebates and federal tax credits with financing lowers your total financed amount and reduces your monthly payment. Stacking incentives from multiple sources, including utility programs, manufacturers, and federal credits, is the most effective way to reduce your total project cost.

Will my energy savings cover my financing payments?

On average, Kansas City homeowners see around 17% lower energy bills even while making financing payments for a new high-efficiency system, though actual results depend on your home size and usage habits.

Is my credit affected if I finance HVAC through my utility?

Utility-based programs like Evergy PAYS® do not require a credit check, and the repayment is structured as a charge on your utility bill rather than as a personal debt reported to credit bureaus.

Recommended

- How HVAC financing works: smart options for KC homes – KC Air Control – Heating & Cooling

- Why upgrade your HVAC? Boost comfort & cut energy bills – KC Air Control – Heating & Cooling

- Smart HVAC budgeting: save money and boost comfort in Kansas City – KC Air Control – Heating & Cooling

- Why upgrade heating systems? Unlock savings and comfort – KC Air Control – Heating & Cooling