TL;DR:

- Using a home equity loan for HVAC upgrades provides fixed payments and predictable budgeting, secured by your home’s equity.

- However, it carries risks like potential foreclosure if payments are missed and requires careful planning to avoid over-borrowing due to closing costs and loan limits.

When your furnace gives out or your air conditioner is running on borrowed time, the question isn’t just “what system do I buy?” It’s “how do I pay for it?” Understanding what is a home equity loan HVAC financing option can change the entire equation. A home equity loan, also called a second mortgage, lets you borrow against the value you’ve built in your home at a fixed rate, making it one of the most predictable ways to fund a major heating or cooling upgrade. This guide walks you through how it works, what it costs, and how to use it wisely.

Table of Contents

- Key takeaways

- What is a home equity loan for HVAC projects?

- Benefits and risks of this financing approach

- How to qualify and apply for the loan

- Practical tips to get the most from your loan

- Comparing home equity loans to other HVAC financing options

- My honest take on using home equity for HVAC

- How Kcaircontrol helps you navigate HVAC financing

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Fixed payments, predictable budget | Home equity loans carry fixed interest rates and set monthly payments for the life of the loan. |

| Your home is the collateral | Missed payments can lead to foreclosure, so borrow only what you can confidently repay. |

| Equity thresholds matter | Most lenders require 15% to 20% equity to remain in your home after borrowing. |

| Plan every cost upfront | The loan is a one-time lump sum. You cannot draw more later without a new application. |

| Tax deductions may apply | Interest can be deductible if the funds are used to substantially improve your home. |

What is a home equity loan for HVAC projects?

A home equity loan is a second mortgage. Your lender gives you a lump sum of money upfront, secured by the equity you hold in your home. You repay it over a fixed term, typically between 5 and 30 years, at a fixed interest rate. The payment stays the same every month, which makes budgeting straightforward.

For HVAC purposes, home equity loans are designed for large, planned expenses like replacing a furnace, installing a heat pump, or upgrading a full central air system. These are exactly the kinds of costs that benefit from a structured, predictable loan rather than a credit card or a short-term personal loan.

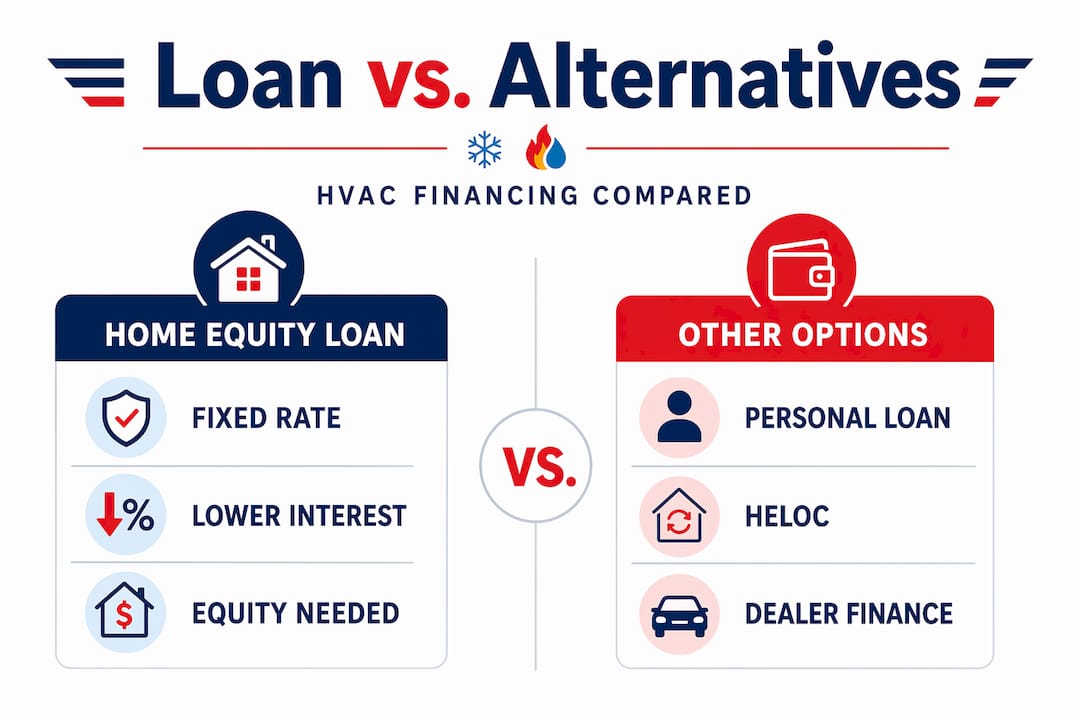

It helps to understand how this differs from a HELOC (Home Equity Line of Credit). A HELOC works like a credit card secured by your home. You draw from it as needed, and the interest rate is usually variable. A home equity loan, by contrast, provides lump sum funds with fixed payments, unlike HELOCs that function as revolving credit lines. For a defined HVAC project with a known cost, that structure tends to work better.

Here is a quick comparison to help you choose:

| Feature | Home equity loan | HELOC | Personal loan |

|---|---|---|---|

| Interest rate | Fixed | Variable | Fixed or variable |

| Disbursement | Lump sum | As needed | Lump sum |

| Repayment term | 5 to 30 years | Draw + repayment period | 1 to 7 years |

| Collateral | Home | Home | None |

| Best for | Planned HVAC replacements | Phased or uncertain projects | Urgent, smaller repairs |

To qualify, lenders typically require you to have enough equity built up. Borrowing limits allow up to 80% to 85% combined loan-to-value against your home’s appraised value minus your existing mortgage balance.

Benefits and risks of this financing approach

The appeal of using home equity for HVAC comes down to predictability and cost. Fixed payments provide solid budgeting for HVAC projects, which is a real advantage when you are managing household expenses alongside a multi-thousand-dollar system replacement. You know exactly what you owe each month from day one.

Home equity loan benefits for HVAC also include cost savings. Home equity loans often carry lower rates than unsecured personal loans or credit cards, which can save you hundreds or even thousands of dollars over the life of the loan if you have strong equity and a solid credit profile.

There is also a potential tax advantage. Loan interest may be tax-deductible when funds are used to buy, build, or substantially improve the qualified residence. A full HVAC system replacement generally qualifies. Partial tune-ups or small repairs likely do not. Keep every invoice and contractor contract if you plan to claim this deduction.

The risks deserve equal attention:

- Foreclosure risk. Because the loan is secured by your home, missed payments put your home at risk of foreclosure. This is a higher stake than an unsecured loan where the worst outcome is damaged credit.

- Closing costs. Closing costs can range from 2% to 5% of the loan amount. On a $20,000 HVAC loan, that is up to $1,000 added to your cost before the first payment is made.

- Fixed amount. If your project goes over budget, you cannot draw more. You would need to apply for a new loan.

- Slower approval. The underwriting process takes time, which makes this a poor fit for urgent breakdowns.

Pro Tip: Before signing any loan documents, calculate the total cost including closing fees, not just the interest rate. A loan with a slightly higher rate and no closing costs can sometimes cost less overall.

How to qualify and apply for the loan

Getting approved for a home equity loan for HVAC upgrades involves several clear steps. Lenders look at four main factors: your credit score, your existing equity, your income stability, and your combined loan-to-value (CLTV) ratio. Most lenders want your CLTV to stay at or below 80%, meaning lenders typically require 15% to 20% equity to remain in your home after the loan closes.

Here is a practical step-by-step process for applying:

- Check your equity. Subtract your mortgage balance from your home’s current estimated value. That difference is your available equity. Use 80% of your home’s value as the ceiling for total borrowing.

- Review your credit score. Most lenders prefer a score of 620 or higher, though better rates go to borrowers at 700 and above.

- Collect HVAC quotes. Get at least two or three detailed quotes from licensed contractors before you apply. You need a concrete number to borrow the right amount.

- Gather documentation. Have recent pay stubs, tax returns, mortgage statements, and your HVAC estimates ready. Lenders will ask for all of it.

- Submit your application. Apply through a bank, credit union, or mortgage lender. The approval process typically takes 3 to 6 weeks, including an appraisal of your home.

- Plan a contingency buffer. Add 10% to 15% to your HVAC estimate when deciding how much to borrow. Unexpected costs during installation are common.

The closed-end nature of home equity loans means you borrow once and cannot return for more funds without starting a new application. Sizing your loan accurately from the start saves you from that situation.

Pro Tip: Ask your lender upfront whether they charge prepayment penalties. If your financial situation improves, paying off the loan early could save you significant interest.

If you want a step-by-step walkthrough tailored to Kansas City homeowners, the HVAC financing application guide from Kcaircontrol covers local lender options and what documents to prepare.

Practical tips to get the most from your loan

Once you decide that home improvement loans for HVAC work for your situation, preparation is what separates a smooth process from a frustrating one. These tips apply whether you are replacing a single unit or upgrading an entire system.

- Get detailed contractor quotes first. Align your contractor budget with your loan amount before applying. Vague estimates lead to under-borrowing or over-borrowing, both of which create problems.

- Keep documentation for tax purposes. Claiming the mortgage interest deduction requires detailed records proving funds improved the home. Save every signed contract, invoice, and payment receipt from your HVAC contractor.

- Set up automatic payments. Delinquency on a secured loan carries consequences that go beyond a late fee. Automating payments protects you from an oversight that could affect your home.

- Plan for the timeline. Home equity loans are not fast. If your HVAC system has already failed and it is the middle of August, you may need a faster financing option while the loan processes.

- Consider HVAC upgrade benefits alongside your financing decision. A new high-efficiency system often reduces monthly energy bills, which can offset part of your loan payment over time.

Pro Tip: If your HVAC need is urgent, ask your contractor about short-term dealer financing to cover the gap while your home equity loan is processing. Just read the terms carefully before accepting.

Comparing home equity loans to other HVAC financing options

Understanding where a home equity loan fits among the best HVAC financing options helps you choose the right tool for your specific situation.

| Financing type | Rate type | Speed | Risk | Best fit |

|---|---|---|---|---|

| Home equity loan | Fixed | 3 to 6 weeks | Home as collateral | Planned full system replacements |

| HELOC | Variable | 2 to 4 weeks | Home as collateral | Phased projects or uncertain costs |

| Personal loan | Fixed or variable | 1 to 3 days | Credit only | Urgent repairs under $10,000 |

| Dealer/contractor financing | Often variable | Same day | Credit only | Point-of-sale convenience |

| Credit card | Variable | Immediate | Credit only | Minor repairs, if paid quickly |

When you can finance HVAC with equity, you generally get the lowest available interest rate and the most predictable monthly payment. That matters on a $15,000 to $25,000 system replacement where even a two-point rate difference can translate to several hundred dollars per year.

Personal loans and dealer financing approve faster and carry no collateral risk. But secured loans like home equity financing carry lower interest rates in exchange for pledging your home. If you are confident in your ability to repay and you have time to plan, the rate advantage is real and meaningful.

For Kansas City homeowners weighing their choices, Kcaircontrol has put together a resource on smart financing options that covers the full picture, including dealer programs and same-as-cash offers worth understanding before you commit.

My honest take on using home equity for HVAC

I’ve seen homeowners approach home equity loans two ways. Some treat them casually, like a quick cash grab for any expense. Others over-research to the point of paralysis and miss the window to get a good rate. Neither approach serves you well.

What I’ve found to be true is that the homeowners who benefit most from this financing method are the ones who treat the application like a project in itself. They get three contractor quotes. They check their credit before applying. They factor in closing costs and size the loan with a buffer built in. That preparation is not complicated. It just requires taking the process seriously before the paperwork starts.

The fixed payment structure is genuinely underappreciated. Unlike a HELOC where your monthly obligation can shift with interest rate changes, a home equity loan gives you one number that does not move. For homeowners managing tight monthly budgets, that certainty is worth more than a slightly lower variable rate that could climb.

The risk is real, though. Your home secures this loan. I would never encourage anyone to borrow against their home for something they cannot comfortably repay. If your financial situation has any uncertainty, a smaller personal loan or contractor financing might be the wiser call even if it costs more in interest.

The homeowners who do this right walk away with a new, efficient system, a payment they planned for, and sometimes a tax deduction to go with it.

— AB

How Kcaircontrol helps you navigate HVAC financing

At Kcaircontrol, we have worked with Kansas City homeowners for over 70 years, and we know that financing is often the hardest part of an HVAC upgrade decision.

Our team can walk you through realistic cost estimates so you borrow the right amount, not more and not less. We provide detailed, itemized quotes that lenders accept directly during the underwriting process. If your system has already failed and you need help fast, our emergency HVAC repair options include financing paths designed for urgent situations where a home equity loan timeline simply will not work. Whether you are planning ahead or dealing with an unexpected breakdown, we are here to help you find the right solution for your home and your budget. Contact us today to schedule a consultation.

FAQ

What is a home equity loan for HVAC?

A home equity loan for HVAC is a second mortgage that provides a lump sum to fund heating and cooling upgrades, repaid at a fixed rate over a set term. It is typically used for planned replacements like furnaces, heat pumps, or full central air systems.

How much equity do I need to qualify?

Most lenders require you to retain 15% to 20% equity in your home after the loan closes, measured by your combined loan-to-value ratio. This means you generally cannot borrow more than 80% to 85% of your home’s appraised value minus your existing mortgage.

Is the interest on a home equity loan for HVAC tax-deductible?

Yes, in many cases. The IRS allows a mortgage interest deduction when funds are used to substantially improve your home, and a full HVAC system replacement typically qualifies. Keep all invoices and contractor documentation to support the deduction.

How long does approval take?

The approval process for a home equity loan typically takes 3 to 6 weeks, which includes a home appraisal and full underwriting review. If your HVAC system needs immediate repair, faster financing options such as personal loans or dealer financing may be more practical while you wait.

Can I finance HVAC with equity if my credit is not perfect?

Most lenders accept credit scores of 620 or higher for home equity loans, though the best rates go to borrowers with scores of 700 and above. If your score is lower, you may still qualify but should expect a higher interest rate and stricter equity requirements.