TL;DR:

- Energy efficiency financing helps homeowners fund HVAC upgrades through loans, mortgages, and incentives to lower energy bills. Various options like dedicated loans, energy-efficient mortgages, and utility rebates allow for affordable, long-term improvement plans. Proper planning, including audits and authorized contractors, can improve approval chances and maximize savings.

Energy efficiency and financing is the practice of funding home upgrades through loans, mortgages, and incentive programs to lower energy bills and improve comfort. For homeowners and property managers, this most often means replacing or upgrading HVAC systems, which are the largest energy consumers in most homes. Programs like Fannie Mae’s HomeStyle Energy Mortgage, Freddie Mac’s GreenCHOICE Mortgage, and the National Energy Improvement Fund (NEIF) give you real, structured paths to pay for those upgrades without draining savings. The right financing option depends on your income, credit, and the scope of the project.

What financing options are available for energy-efficient HVAC upgrades?

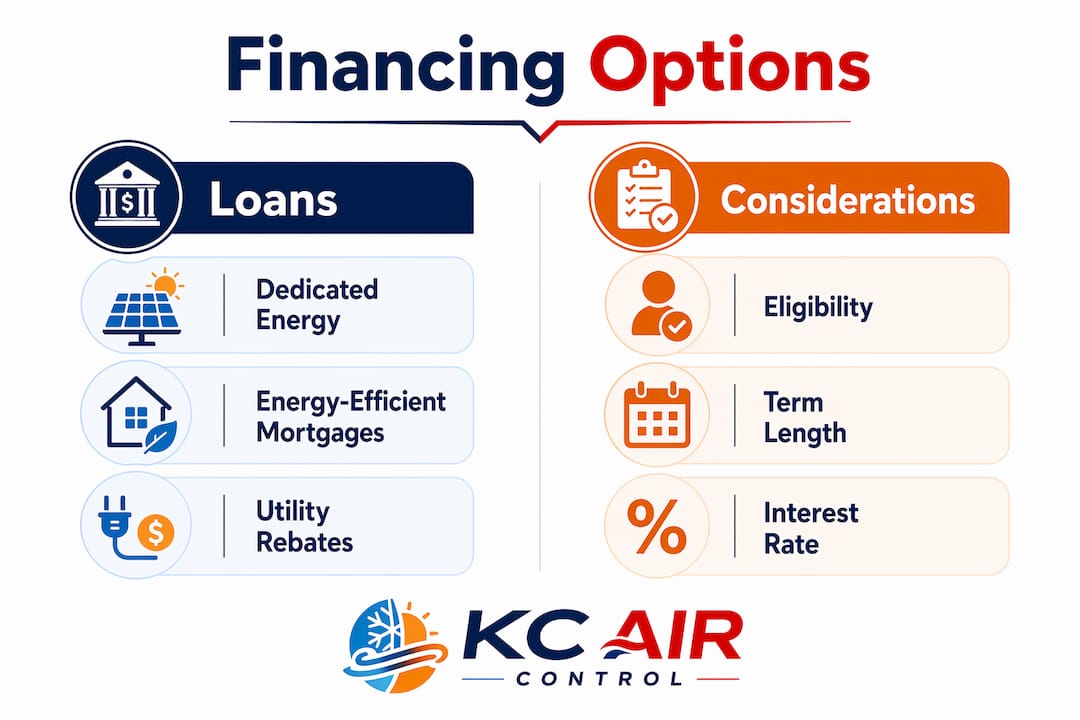

Green energy financing options fall into four main categories: dedicated energy loans, energy-efficient mortgages, government and utility incentives, and on-bill or PACE programs. Each works differently, and knowing the distinctions saves you time and money.

Dedicated energy savings loans are the most direct route. Programs like Colorado’s RENU and NEIF’s EnergyPlus offer loans from $2,500 to $75,000 with terms up to 20 years and no money down. Some include a 0% APR introductory period of 12 months. That combination of size and flexibility covers everything from a basic furnace replacement to a full HVAC system overhaul.

Energy-efficient mortgages (EEMs) integrate upgrade costs directly into a home purchase or refinance. The U.S. Department of Energy confirms that EEMs offer lower interest rates than unsecured personal loans and allow higher mortgage approval amounts because lenders factor in the energy cost savings that offset monthly payments. If you are buying a home or refinancing anyway, this is the most cost-effective path.

Government and utility incentives include rebates, grants, and subsidies that reduce your upfront cost before financing even enters the picture. Some programs stack: you can apply a utility rebate, then finance the remaining balance through a low-interest energy loan. Check with your local utility and state energy office for current offers, since these programs change frequently.

On-bill financing and PACE programs let you repay upgrade costs through your utility bill or property tax assessment. PACE (Property Assessed Clean Energy) is especially useful for property managers because the obligation transfers with the property at sale.

- Dedicated energy loans: $2,500–$75,000, terms up to 20 years, often unsecured

- Energy-efficient mortgages: lower rates, higher borrowing limits, tied to home purchase or refi

- Government rebates and grants: reduce upfront cost, often stackable with loans

- On-bill financing: repayment through utility bill, no separate loan payment

- PACE programs: repaid through property taxes, transferable at sale

Pro Tip: Before applying for any loan, call your utility company first. Many utilities offer rebates of $200–$1,000 on qualifying HVAC equipment, and stacking that rebate with a low-interest loan cuts your total financing need significantly.

How do energy efficiency financing programs work?

Most financing programs for energy upgrades follow a structured process, and understanding it upfront prevents delays. The steps below reflect how the majority of dedicated energy loan programs operate.

- Find an authorized contractor. Most programs require that a contractor enrolled in the financing program initiates your application. You cannot apply directly as a homeowner. Kcaircontrol works with financing programs, so ask about enrollment when you schedule your consultation.

- Schedule a home energy audit. Lenders and program administrators require proof that the upgrade will deliver real savings. Home energy audits using ratings like HERS or the DOE Home Energy Score calculate projected savings and confirm cost-effectiveness. This step is non-negotiable for most programs.

- Choose your loan type. Unsecured energy loans skip the property lien and appraisal required by home equity loans, which means faster approval. If speed matters, an unsecured loan is the better choice.

- Submit the application through your contractor. Your contractor submits project details, the audit results, and your financial information. Approval timelines vary by program but are typically faster than traditional home equity products.

- Complete the upgrade and verify. Many programs require a post-installation inspection to confirm the work meets program standards before funds are fully released.

Eligibility criteria vary by program. Income limits apply to some subsidized loans. Credit score thresholds apply to most unsecured products. Project cost-effectiveness, meaning the upgrade must save more than it costs over its life, is a requirement across nearly all programs.

Pro Tip: Request your HERS rating before you start shopping for loans. A lower HERS score (better efficiency) strengthens your application and may qualify you for better terms.

Comparing the top financing options for HVAC upgrades

The table below compares the major financing types available to homeowners and property managers in 2026.

| Financing type | Loan amount | Term | Interest rate | Collateral required | Best for |

|---|---|---|---|---|---|

| NEIF EnergyPlus / RENU | $2,500–$75,000 | Up to 20 years | Low to 0% intro APR | No | Standalone HVAC upgrades |

| Energy-efficient mortgage (EEM) | Tied to home value | 15–30 years | Below market rate | Yes (home) | Buyers or refinancers |

| PACE program | Varies by project | 5–25 years | Fixed, varies by state | Property tax lien | Property managers, investors |

| Utility on-bill financing | Typically under $10,000 | 3–7 years | Low to 0% | No | Smaller upgrades, appliances |

| Government grants and rebates | Up to $4,000 (varies) | N/A (not a loan) | N/A | No | Low-to-moderate income households |

A few points deserve emphasis. EEMs allow you to qualify for higher loan amounts because lenders count projected energy savings as income. That is a real advantage if you are close to a borrowing limit. PACE programs are powerful for property managers because the debt attaches to the property, not the person. If you sell, the new owner assumes the obligation.

Solar and battery systems illustrate the payback math clearly. Systems costing $10,000 to $40,000 typically pay off in about 7 years through energy savings. Government subsidies can cut that payback period to as little as 4 years. That math makes financing energy upgrades a sound financial decision, not just an environmental one.

For homeowners who want to understand the full picture of why HVAC upgrades pay off, the savings case is strong even before financing incentives are applied.

Tips for maximizing your energy upgrade financing

Getting the financing right matters as much as choosing the right equipment. These are the mistakes homeowners most commonly make, and how to avoid them.

- Skip the audit, lose the loan. Many homeowners assume they can apply for financing and schedule the audit later. Most programs require the audit before approval. Book it first.

- Do not ignore income-based programs. Programs like New South Wales’s Home Energy Saver offer zero-interest loans up to $15,000 and discounts up to $4,000 for qualifying households. Similar income-targeted programs exist across U.S. states. If your income qualifies, these programs are far better than market-rate loans.

- Stack incentives before financing. Apply every rebate and grant you qualify for first. Finance only what remains. This reduces your loan principal and total interest paid.

- Match loan term to equipment life. A furnace lasts 15–20 years. A loan term of 20 years aligns with that life. Do not take a 7-year loan on a 20-year asset if the monthly payment strains your budget.

- Check contractor authorization before hiring. Authorized contractors initiate applications for most specialized programs. Hiring an unauthorized contractor locks you out of those programs entirely.

Pro Tip: Ask your contractor specifically which financing programs they are enrolled in before signing any agreement. A contractor enrolled in NEIF, Michigan Saves, or a state clean energy fund opens doors that a non-enrolled contractor cannot.

Financing energy upgrades also raises your home’s value. An energy-efficient HVAC installation is one of the highest-return improvements you can make before listing a property. Buyers increasingly factor energy costs into purchase decisions, and a documented, financed upgrade signals a well-maintained home.

For a detailed walkthrough of the loan application process, the step-by-step HVAC loan guide from Kcaircontrol covers each stage from audit to approval.

Key Takeaways

Combining energy savings loans, government incentives, and the right contractor access is the most effective way to finance HVAC upgrades while minimizing out-of-pocket costs.

| Point | Details |

|---|---|

| Start with incentives, then finance | Apply rebates and grants first to reduce the loan amount you need. |

| Authorized contractors unlock programs | Most specialized energy loans require a program-enrolled contractor to initiate your application. |

| Energy audits are required, not optional | HERS ratings and DOE Home Energy Scores are mandatory for most loan qualifications. |

| Unsecured loans mean faster approval | No property lien or appraisal speeds up the process compared to home equity products. |

| EEMs allow higher borrowing | Lenders count projected energy savings as income, raising your eligible loan amount. |

What I have learned about energy financing after years in the field

The gap between what homeowners think financing looks like and what it actually requires is wider than most people expect. The most common assumption I see is that you can shop for equipment, pick a loan, and get started. The reality is that the best programs, the ones with zero interest or long terms, require you to work backward. You need the contractor first, then the audit, then the loan.

The other thing that surprises homeowners is how much lender hesitation still exists in this space. Financial institutions often perceive energy projects as risky because of small transaction sizes and limited capacity to evaluate energy savings. That is why Energy Service Companies (ESCOs) exist. ESCOs combine financing with technical expertise to make projects bankable that a traditional lender would decline. If you are managing a larger property or a commercial space, an ESCO relationship is worth exploring through resources like government incentive programs that support residential and commercial energy improvements.

My honest advice: treat the financing decision with the same care you give the equipment decision. A great heat pump on a bad loan is still a bad deal. A modest system on a zero-interest, 20-year term can deliver better financial outcomes than a premium system financed at 9%. Run the numbers on total cost, not monthly payment.

— AB

Kcaircontrol can help you put it all together

Financing an HVAC upgrade is straightforward when you have the right partner. Kcaircontrol brings over 70 years of experience serving Kansas City homeowners, and we understand both the equipment side and the financing side of the equation.

Whether you need a new furnace, a full system replacement, or guidance on which financing programs apply to your home, our team walks you through every step. We work with financing programs that make quality HVAC upgrades accessible without large upfront costs. If your system is showing signs it needs repair or replacement, now is the right time to explore your options. Contact Kcaircontrol to schedule a consultation and find out which financing programs your project qualifies for.

FAQ

What is energy efficiency financing for HVAC systems?

Energy efficiency financing covers loans, mortgages, and incentive programs that fund HVAC upgrades to reduce energy costs. Options include dedicated energy loans, energy-efficient mortgages, and government rebates.

Do I need a home energy audit to qualify for an energy loan?

Most programs require a home energy audit using ratings like HERS or the DOE Home Energy Score before approving a loan. The audit confirms that the upgrade will deliver measurable savings.

Can I apply for an energy efficiency loan directly?

Most specialized programs require an authorized contractor to initiate the application on your behalf. Hiring a contractor enrolled in programs like Michigan Saves or NEIF is the first step.

What loan amounts are available for home energy upgrades?

Programs like NEIF’s EnergyPlus and Colorado’s RENU offer loans from $2,500 to $75,000 with terms up to 20 years. Some programs also offer 0% APR introductory periods of 12 months.

How do energy-efficient mortgages differ from standard home loans?

Energy-efficient mortgages integrate upgrade costs into a home purchase or refinance and typically offer lower interest rates than unsecured loans. Lenders also allow higher borrowing amounts because projected energy savings offset monthly payments.