TL;DR:

- Many homeowners mistake “same as cash” HVAC offers for free financing, risking costly charges if deadlines are missed. These plans often accrue interest silently during promotional periods, and missing the deadline can result in paying retroactive interest amounts that vastly increase total costs. To avoid surprises, it is essential to understand the difference between deferred-interest plans and true 0% financing and to track payments carefully before the deadline.

Many Kansas City homeowners see “same as cash” in an HVAC offer and assume it means completely free financing. That assumption is understandable but often costly. These offers are structured in a way that favors lenders when customers miss a single deadline, and the resulting charges can catch you completely off guard. This guide explains exactly how same-as-cash HVAC financing works, where the real risks live, and what steps you can take to protect your wallet while still getting the comfort upgrade your home needs.

Table of Contents

- What is same-as-cash HVAC financing?

- Deferred interest vs. true 0% financing: What’s the difference?

- Common mistakes and how to avoid the deferred interest trap

- When does same-as-cash HVAC financing make sense?

- A homeowner’s perspective: Why fine print matters more than you think

- Explore HVAC financing and repair solutions in Kansas City

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Deferred interest warning | Most same-as-cash offers build interest that becomes due if the balance isn’t paid in full by the deadline. |

| Critical paperwork details | Never assume 0% means zero risk—always read the fine print for retroactive interest clauses. |

| Minimum payments risk | Paying only the minimum won’t clear the balance in time and often leads to costly interest charges. |

| When it works | Same-as-cash HVAC financing is best for those who can pay the full amount before the promo period ends. |

| Explore all options | Compare financing solutions and choose the fit that aligns with your budget and payment ability. |

What is same-as-cash HVAC financing?

Same-as-cash HVAC financing sounds straightforward, but the term can mislead you if you read it too quickly. Most people picture a genuine 0% loan where no interest builds up at all. The reality is often different.

Deferred-interest financing means the lender advertises 0% during the promotional period, but interest typically accrues the whole time and becomes fully owed if you do not pay the balance in full before the window closes. The key word here is deferred: interest does not disappear, it waits. If you meet the deadline, you pay nothing extra. If you miss it, even by a single day, all of that accumulated interest lands on your account at once.

You can explore HVAC financing options for Kansas City homes to get a clearer picture of what is available locally. Before committing, understanding the structure of the offer is essential.

How a typical same-as-cash offer works:

- A lender or HVAC contractor presents a promotional period, commonly 6, 12, or 18 months.

- During that window, no interest payments are required.

- Interest silently accrues on the original balance throughout the promo period.

- If the balance is paid in full before the deadline, all accrued interest is waived.

- If even a small balance remains at the deadline, all accrued interest is applied immediately.

Here is a quick look at how promotional timelines typically compare:

| Promo Period | Balance Example | Interest Rate (Accruing) | Interest Owed If Missed |

|---|---|---|---|

| 6 months | $3,000 | 26.99% APR | ~$400+ |

| 12 months | $5,000 | 26.99% APR | ~$1,350+ |

| 18 months | $8,000 | 26.99% APR | ~$3,240+ |

These numbers illustrate why missing the deadline is not a minor issue. A $5,000 HVAC installation could suddenly cost you $6,350 or more with no warning, simply because you did not clear the balance in time. Reviewing HVAC budgeting tips before signing any financing agreement can help you plan your payments realistically.

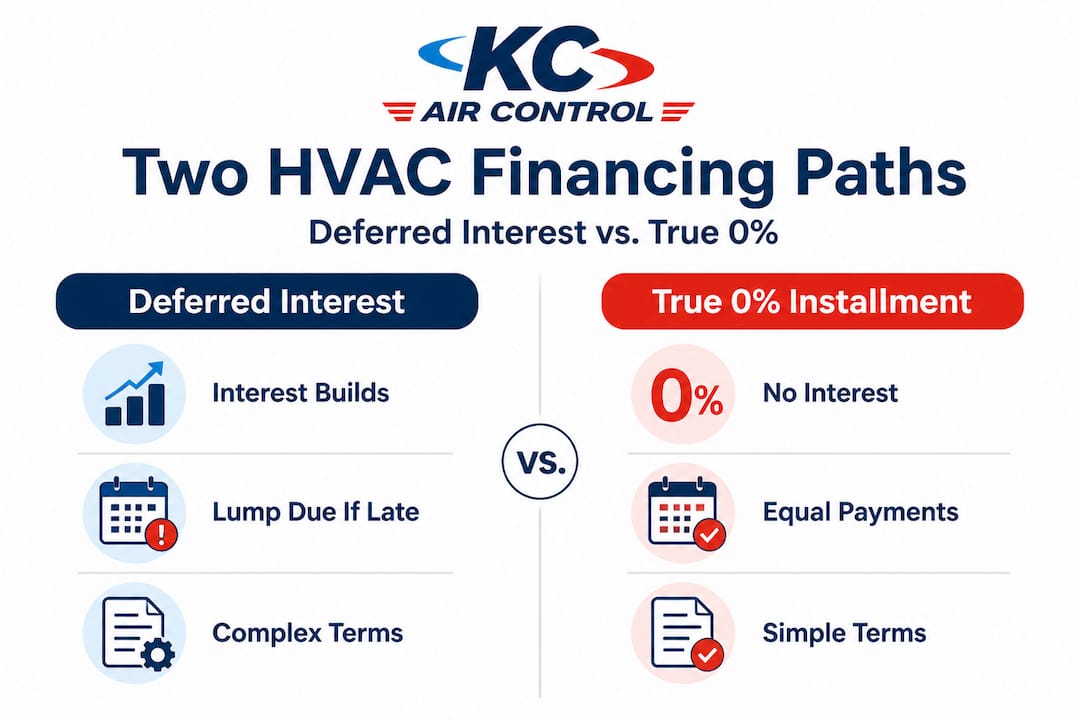

Deferred interest vs. true 0% financing: What’s the difference?

With the basics in place, it is crucial to understand the fundamental difference between deferred-interest plans and true 0% offers.

True 0% installment financing means no interest builds at all during the promotional window. Equal payments are spread across the term, and if you miss the deadline on a true 0% plan, you simply move to the standard going-forward rate, not a retroactive pile of charges. Deferred-interest offers are commonly paired with phrases like “no interest if paid in full,” which signals that interest is running in the background the entire time.

The marketing language between these two products looks almost identical. That is by design, and it means you need to read every word of the financing paperwork before signing.

| Feature | Deferred-Interest (Same as Cash) | True 0% Installment Financing |

|---|---|---|

| Interest accrues during promo? | Yes, silently | No |

| Retroactive interest if missed? | Yes, all at once | No |

| Monthly payment structure | Minimum only (risky) | Fixed equal payments |

| Risk of surprise charges | High | Very low |

| Deadline flexibility | None | Low stakes |

Pro Tip: Search for the exact phrases “deferred interest” or “no interest if paid in full” in your loan paperwork. If you see either phrase, you are dealing with a deferred-interest plan, not a true 0% product. They look similar in ads but behave very differently when a deadline is missed.

Important decision rule: Treat same-as-cash offers as deferred interest unless the paperwork explicitly states true 0% with no retroactive or deferred-interest consequence if you miss the payoff date. If the paperwork is unclear, ask the lender directly in writing before you sign.

When you are applying for HVAC financing, request a clear statement from the lender explaining what happens if you miss the promotional payoff deadline. A lender offering a legitimate true 0% product will answer that question directly and without hesitation. One offering deferred interest may use vague language, which is itself a signal.

Understanding choosing the right HVAC system is also part of this process. A more energy-efficient system may cost more upfront but saves money monthly, which affects how quickly you can pay off any financing balance.

Common mistakes and how to avoid the deferred interest trap

Knowing these risks, let us look at real mistakes homeowners make and how you can sidestep the trouble.

The single most common mistake is making only minimum monthly payments. Minimum payments on a deferred-interest plan are calculated by the lender to keep the account current, not to guarantee the balance is cleared by the promotional deadline. Paying only the minimum usually does not pay off the promotional balance before the end date, and the payoff amount and deadline matter far more than the minimum due.

Here is a real-world example. You finance a new furnace and AC system for $6,000 on an 18-month same-as-cash plan. The minimum monthly payment is $50. After 18 months of minimum payments, you have paid only $900, leaving $5,100 on the balance. All accrued interest from 18 months applies immediately. That single missed deadline cost you thousands of dollars in a situation where you genuinely believed you were following the rules.

Five steps to avoid the deferred interest trap:

- Calculate your true monthly payoff amount. Divide the full balance by the number of months in the promo period. That is the amount you need to pay each month, not the lender’s minimum.

- Mark the promo deadline on your calendar. Set a reminder at least 60 days before the deadline so you have time to make a final lump-sum payment if needed.

- Track every payment you make. Keep a simple spreadsheet or notes app record showing what you have paid and what remains. Do not trust the lender’s statement alone.

- Get payoff confirmation in writing. One month before the deadline, contact your lender and request written confirmation of your exact payoff amount and the specific due date.

- Watch for deferred interest resets. Some plans reset the promo clock if you miss a payment or pay late. One missed payment can trigger an early end to your promotional period.

Pro Tip: Call your lender, not just check their website, to confirm your payoff figure and exact deadline about 45 to 60 days before the end of your promotional period. Ask them to send a written confirmation by email or mail. This one step prevents most deferred interest disasters.

Staying on top of HVAC maintenance also plays a role here. A well-maintained system is less likely to need emergency repairs while you are still paying off your installation, which protects your cash flow and helps you stick to your payoff plan.

When does same-as-cash HVAC financing make sense?

Understanding what to avoid leads to the practical question: when does this type of financing actually work for you?

Same-as-cash financing is genuinely useful in specific, well-defined situations. It can be cost effective for HVAC upgrades if and only if you are fully prepared to pay the promotional balance by the deadline. The key word is “prepared,” not just “planning to.”

Same-as-cash financing works well when:

- You are expecting a tax refund, year-end bonus, or insurance payout that will cover most or all of the balance well before the deadline.

- You have the cash available now but prefer to keep it liquid for a specific short-term reason, such as an emergency fund, and you will move it over before the deadline.

- The promo period is short enough that your calculated monthly payment fits comfortably in your budget.

- You have a strong track record of paying financing accounts on time with no missed payments.

Same-as-cash financing carries higher risk when:

- Your income is irregular or seasonal, making it hard to guarantee payments every month.

- You are financing a large balance over a long promo period and the required monthly payoff amount is a stretch.

- You already carry other financial obligations that compete for the same cash each month.

- You are counting on a future event, like a bonus or tax refund, that is not guaranteed.

If you are in the higher-risk category, other HVAC financing options may serve you better. Here are alternatives worth asking about:

- True 0% installment loans from credit unions or local banks with fixed equal payments and no retroactive interest

- Home equity line of credit (HELOC) using your home’s equity at a lower fixed or variable rate

- Traditional personal loans with a predictable fixed rate and clear monthly payment

- Credit union HVAC programs that offer competitive rates with no deferred-interest trap

- Manufacturer or utility rebate programs that reduce the total amount you need to finance in the first place

Matching your financing to your actual cash flow, not your best-case cash flow, is what protects you long term. Comfort upgrades should improve your home life, not create financial stress.

A homeowner’s perspective: Why fine print matters more than you think

Here is where most homeowners and even some experienced buyers get caught out, and what we have seen repeatedly over decades of working with Kansas City families on HVAC decisions.

The marketing around same-as-cash offers is designed to feel safe. Words like “no interest” and “same as cash” signal a fair deal. But lenders who offer these products understand that a significant percentage of customers will not meet the deadline. That reality is built into the business model. These promotions are structured to be lucrative specifically because missed deadlines generate large, retroactive interest charges.

Conventional wisdom says to grab 0% financing whenever it is available. That advice is correct only when the product is genuinely 0% with no retroactive consequence. With deferred-interest plans, the calculus is completely different. The risk is not just paying more; it is paying months of back interest all at once, often at rates between 26% and 30% APR.

The hard-won lesson is this: no reminder system is overkill. Set calendar alerts, use a payment tracking app, call your lender at the 60-day mark, and make your final payment a week early, not the day of the deadline. Lenders process payments on business days, and a weekend deadline with a Friday payment can land you one business day late.

What most guides miss is that lenders make these offers attractive by betting customers will not track the details. The people who come out ahead with same-as-cash HVAC financing treat it like a disciplined savings goal, not a passive financial arrangement. You can read about real homeowner financing stories to see how preparation made the difference. When you go in with a clear plan and specific numbers, these offers can genuinely work in your favor.

Explore HVAC financing and repair solutions in Kansas City

Now that you understand how same-as-cash works, you are in a much stronger position to make a smart decision for your home.

At KC Air Control, we have been helping Kansas City homeowners navigate HVAC upgrades, repairs, and financing options for over 70 years. We can walk you through HVAC financing options in Kansas City that fit your budget and your timeline, including same-as-cash plans, true 0% programs, and flexible alternatives. Whether you need a new system, furnace repair, or an indoor air quality upgrade, our team is here to help you find a solution that keeps your home comfortable without financial surprises. Reach out or schedule a consultation today to talk through your options with a trusted local expert.

Frequently asked questions

Is same-as-cash HVAC financing really 0% interest?

It usually means no interest is charged if you pay the full balance by the promotional deadline, but interest accrues throughout the promo period and is owed in full if you miss that date.

What happens if I don’t pay off my same-as-cash HVAC loan in time?

All accrued interest from the start of the promotional period may be added to your balance at once, making the total cost of the loan significantly higher than expected.

Is it better to take a traditional loan or same-as-cash for HVAC upgrades?

It depends on your ability to pay off the promo balance before the deadline. Traditional loans offer more predictable fixed payments with no risk of retroactive interest charges, making them a safer choice for many homeowners.

How can I avoid owing retroactive interest on HVAC financing?

Calculate the exact monthly payment needed to clear the balance by the deadline and always pay that amount, never just the minimum payment, and confirm your payoff figure in writing with your lender before the end date.

Are same-as-cash HVAC plans available all year in Kansas City?

Promotions vary by contractor and lender, so the availability and terms of same-as-cash offers can change throughout the year. Check with your provider directly for current options and any time-sensitive offers.

Recommended

- How HVAC financing works: smart options for KC homes – KC Air Control – Heating & Cooling

- How to Apply for HVAC Financing: Kansas City Guide – KC Air Control – Heating & Cooling

- HVAC maintenance affects financing for Kansas City homes – KC Air Control – Heating & Cooling

- HVAC impact on Kansas City rentals: comfort, compliance, ROI – KC Air Control – Heating & Cooling

- AI SEO for HVAC Contractors in Canada — Locally Visible